I’ve never been much into reading books. The last novel I read was probably required reading during a high school literature class. I’ll occasionally pick up a biography, history, or business book. Since nerding out on personal finance, I’ve been scouring blogs, case studies, IRS code, etc on the subject, but The Simple Path to Wealth is honestly the first full personal finance book I’ve read. I liked it enough that I’ve started recommending it to everyone I know and even gave a copy to a friend. I want to give my thoughts on it and, based on what I learned, will have to revisit some of the subjects I’ve already posted about.

Background

The author, JL (Jim) Collins, is well-respected in Financial Independence circles and is identified as one of the original motivators for many FI bloggers, like Mr Money Mustache and the Mad Fientist. Much of the book’s content can also be found via the Stock Series on his blog. The content came about out of a desire to help his daughter set herself up for financial freedom upon graduating from college. It’s focused on keeping things SIMPLE! Consequently, he does not direct his audience to risky and complicated investments like penny stock investing, flipping businesses, real estate investment, or trading currencies.

The book is written simple enough that someone with no investing experience could walk away with a good sense of how and why to invest. It should also make it clear that if you live frugally, invest wisely, and stay the course, building wealth is incredibly easy!

Takeaways

In a few words, here are what stood out as the basic messages from the book: becoming a millionaire should be easy, invest at least 50% of your income, everyone needs F-you money, don’t take on debt, don’t try to beat or time the market, the market will always rise in the long run, use Vanguard, all you need is VTSAX, find a substitute for VTSAX if it’s not available to you, index funds are self-cleansing (the losers like Enron fall out and are replaced), financial advisors need you a lot more than you need them, identify what’s important to you and it don’t let it be showing off to your peers, learn the basics of tax code, learn about safe withdrawal rates, and you can retire comfortably whenever you want.

Although some of those messages won’t sound new, Jim provides a lot of support for why they are accurate and how to accomplish them.

My Thoughts

I’m not going to dive deep into any particular section. I encourage everyone to read the book (or at least start with his Stock Series blog to get a taste), and Jim will do a better job at expounding than I could.

However, I will share a few things that were profound to me.

- You don’t always get what you pay for. You could be paying 0.25% in 401(k) fees (like my wife does), while your neighbor is paying 2%. Odds are, the 2% fee isn’t getting you any better performance, just higher costs. Check your plan and funds to see what you’re getting charged. If you have a financial advisor, odds are they’ll put you into expensive, managed mutual funds plus charge you a management fee. Between those expenses, they’d have to outperform the market by about 2% for you to come out ahead. That is extremely tough to do, and you’ll be hard-pressed to find someone that consistently does it. If you remember the rule of 72, at 9% return, it takes 8 years to double your money. A 2% fee leaves you with a 7% return, so 10.28 years to double your money. With a $100,000 investment at age 40, almost one less doubling event by age 72 would mean ~$900k instead of $1.6 mil!

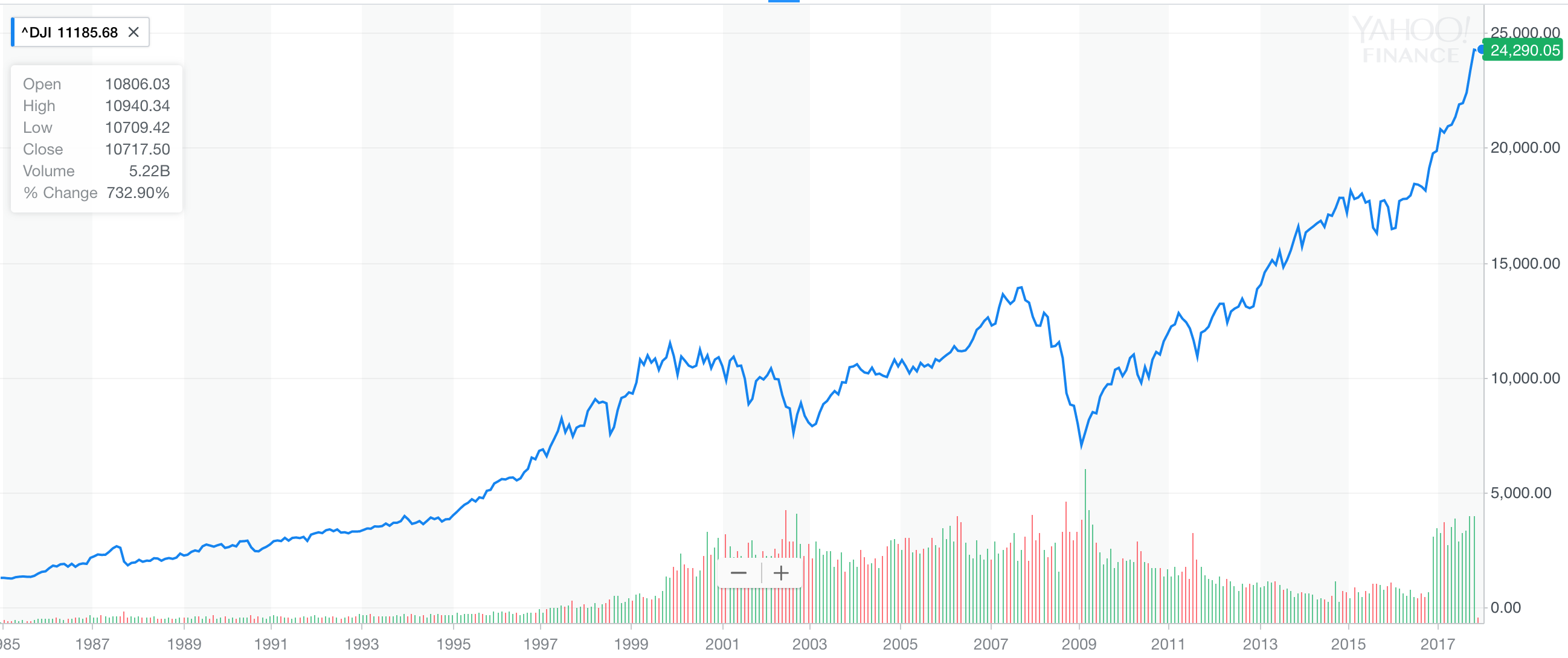

- The Market will ALWAYS go up. Sure there are scary times when the market drops and you think your life is over, but now that it’s 2017, I wish I could buy at 2007 prices! Not convinced? The chart below shows the Dow Jones index from 1985 to present. In the book, Collins speaks of when the market dropped 500 points in one day in 1987. Soon after, he panicked and sold. Doesn’t look like a big deal 30 years later, does it? Occasionally, the market WILL DROP and you WILL LOSE BIG, but rest assured that it WILL GO BACK UP and you’ll wish you would have bought more.

- Be aware of your tax situation. There isn’t a straight answer for everyone here. But be aware of the tax implications and loopholes with each of the retirement buckets (401k/IRA, Roth 401k/Roth IRA, Taxable). The Mad Fientist wrote a great summary about this that both Collins and I recommend. Access Retirement Funds Early

- Find your safe withdrawal rate. I wrote a post about the 4% Rule. I’ll need to write a new post about this, because I think for most early retirees a 5% rule is still pretty safe. That means I can retire even sooner. The book references this study about safe withdrawal rates. Review the study, and you’ll be impressed.

Buy the book, read it, leave your comments, and prosper!

Pingback: My quick plan for financial independence | Salary Optional