If you’re not familiar with the term credit card churning, here is a quick summary: you apply for multiple credit cards, get all their sign-up bonuses, pay them off, and close them (often before getting charged annual fees). I’ve churned through several credit cards and will probably go through several more. There are a lot of gotchas that you should be aware of before you get too deep:

Why do it?

How much can you make?

On my best credit card bonus, I made $1500. There are plenty that can get you $400 cash or a roundtrip flight to Paris ($1300). How about getting a free companion ticket for every time you fly? Pretty easy to get $500/year opening up 1 checking and 1 savings account. It’ll take you all of 10 mins to do online, and maybe an hour to switch direct deposit and go in the branch to close your account.

The money is real!

What will happen to my credit score?

There is no one surefire answer to this, but I think there are some guidelines to live by. When you get a new credit card, a few things happen:

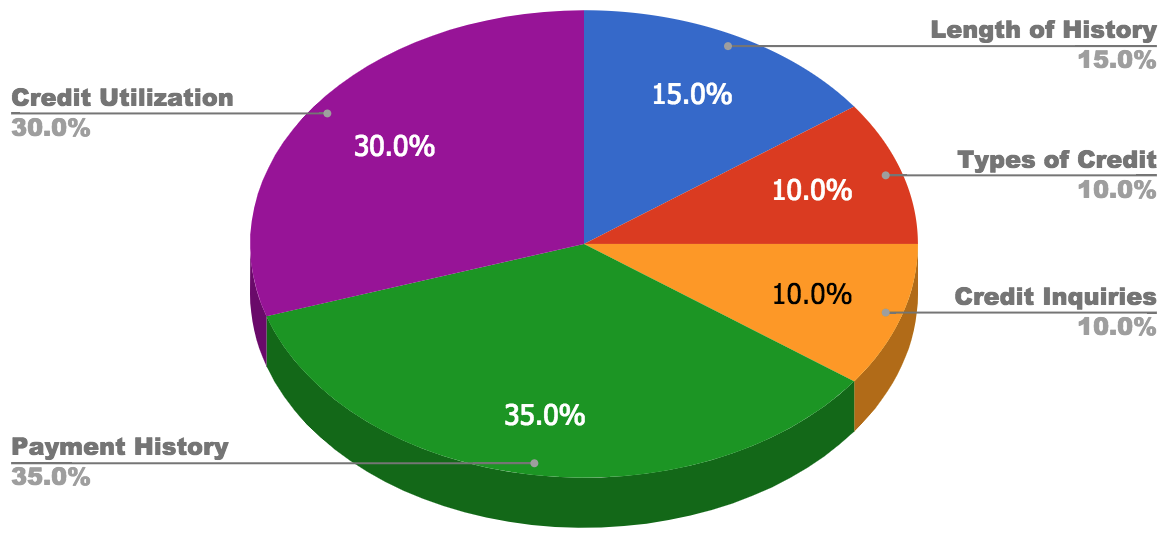

A credit inquiry is added to your credit report 👎

Your available credit increases, so your credit utilization goes down 👍

Your average account history length decreases 👎

According to FICO, here’s how those elements play into your credit score:In my experience, my credit score goes down a few points immediately after I apply for the card. Within a couple months of paying it off in full, my credit score bounces back up to my original score. Kinda makes sense to me… The inquiry and length of history gets knocked (25% of score), but my credit utilization and payment history improves (65%). When I close cards, I never really notice an impact. That could be because I keep credit utilization really low and have plenty of other types and history that those little things don’t much matter. I keep a close eye on my credit report via programs like Credit Karma, so I am not too worried about the affects of churning at this point.

That being said, I keep my churning at bay for a few months if I’m going to be getting a new mortgage.

There are also some premium credit cards (like Chase Sapphire Reserve) that say they won’t approve those having more than 5 credit inquiries in the last year. Not necessarily a ding to your credit score but can prevent your ability to get new credit.

Why not to do it?

This list could be long, but I’ll try to abbreviate…

It can be hard to manage lots of cards simultaneously. You gotta keep track of payments, make sure you get your bonuses, watch for fraud on unused cards, and remember to cancel before you get charged an annual fee. Checking in regularly through programs like Personal Capital or Mint make this easier.

Open too many cards at once, and you have to overspend. A friend of mine opened 3 cards at once to get all the sign up bonuses. Then to get the bonuses, he had to spend $10k total on those cards in 3 months. Then you’re trying to find ways to spend money just to earn a bonus. Not good. If you do get stuck, consider buying gift cards that you know you’ll use.

You may be wasting your only chance to get the bonus. What do I mean by this? There are several cards that have this to say about their sign-up bonus. So if you ever want this same bonus in the future, you may never be eligible for it again. So if you apply for every credit card bonus imaginable now, you may be limiting your options for the future. That being said, I’ve had a few cards that said the sign up bonus was good once in a lifetime, but after I canceled, they invited me to apply again in the future. Other credit cards may have this type of restriction: In this situation, you could apply for the card, earn your bonus, cancel it, and then apply again in 2 years and get the bonus again.

“With great power comes great responsibility.” If you’re prone to overspend or get into credit card debt, avoid churning at all costs! I definitely have more available credit than I have use for. I once bought a car on a credit card, because they wouldn’t give me any further discounts using cash/check. Put that purchasing power into the wrong hands, and someone could get in a lot of trouble.

Churning isn’t just for credit cards

There are plenty of other products you can churn, like checking and savings accounts. My wife and I have each opened 3-4 checking accounts with Key Bank, just for the sign up bonuses. Check out latest promos here. We wait for one of their $300-$400 deals comes around, switch our direct deposit over, then close it 6 months later. Everyone has probably seen the Chase checking and savings deals in the mail or online. We maintain an account there, but probably once a year I’ll open up a savings account, put $15k in, get $250 bonus, then transfer my money out. HSBC, TD, and US Bank regularly have these deals too. Another great thing… after you’ve had and canceled accounts, these places tend to send you great offers to get you back.

Point is, it’s pretty easy to make an extra $1000 (double if you and a spouse play the game) per year by spending less than 5 hours per year.

Bottom Line

Churning has become a habit and game for me, but it’s not for everyone. Read the fine print, so you know how to get your bonus, how to avoid fees, how long you need your account open, etc. Know that your checking and savings bonuses will get taxed as ordinary income come tax season. Credit card bonuses won’t be taxed.

Keep your eyes peeled for good bonuses, and you’ll make some easy money and fund your next vacation or two!