The banking and investment worlds are full of fees. I really learned this while working at Wells Fargo. Boy did they charge fees! Some avoidable, some inevitable. Just want a checking account (no savings or credit card)? $10/month fee. Sending a wire transfer? $35 fee. Receiving a wire? $15 fee. Want your credit card to fund overdrafts? $20 fee every time. Some think fees are only problems for those that can’t manage their money. Well if you have a million bucks, expect fees to be more extreme. Now there’s more for the taking, and you can bet financial advisors will salivate over getting a piece of it. If you use a financial advisor to manage $1,000,000, odds are you’ll pay at least $10,000/year in advisor fees. Do you think they are providing at least $10,000 of value each year? It can be very hard to tell! Imagine how that $10,000/year adds up over 30 years.

How advisors are paid

Although there are many hard-working, well-intentioned financial advisors, commission structures are usually in opposition to the interest of the client. Financial advisors are usually paid with one or both of the following structures:

- Management Fee with Assets Under Management (AUM) model – Personal Capital did a study of management fees across various institutions. You should click that link and look at the graph. Yowza! Not sure why Fidelity wasn’t on there, but they at least have the guts to publish their fee schedule. Although there is much variability, let’s call 1% a typical management fee. This means that if you have $100,000 in your account, you’ll get charged $1,000 every year for your financial advisor. I feel really bad for anyone at those pricey ones charging 2.5%. Yikes! Do you think these advisors will beat the market by at least 2.5%? Odds are they won’t.

- Trade Commissions/Load Fees – Often advisors have products they are paid to sell. For example, an Ameriprise financial advisor may get paid 2.5% for selling you a specific mutual fund like IBALX. Let’s say this has a “load fee” of 5%. You buy $10,000 of this fund, pay a 5% load fee/commission of $500 and your financial advisor collects $250 (2.5% commission). This incentivizes your advisor to put you into expensive products AND to trade them frequently. The more they trade your money, the more they get paid with your money. Do you think these funds pay out more than a low cost funds like VTSAX or a Vanguard Target Retirement fund? Odds are they don’t!

It is not unusual for advisors to charge BOTH of the above fees. Ya, it can be expensive!

Fund Management Fees

In addition to your advisory fees, all mutual funds and ETFs have expenses too. When analyzing a fund, you’ll see this called an expense ratio. If you’re wanting an S&P 500 index fund, it doesn’t make much sense to buy one with a 1.2% expense ratio when you could buy one that has a .04% expense ratio. The two funds should contain nearly the same basket of stocks. Choosing the latter should give you .98% better growth every year. Many actively managed mutual funds (ones advisors will select for you) have expense ratios around 1%.

How Fees Impact Growth

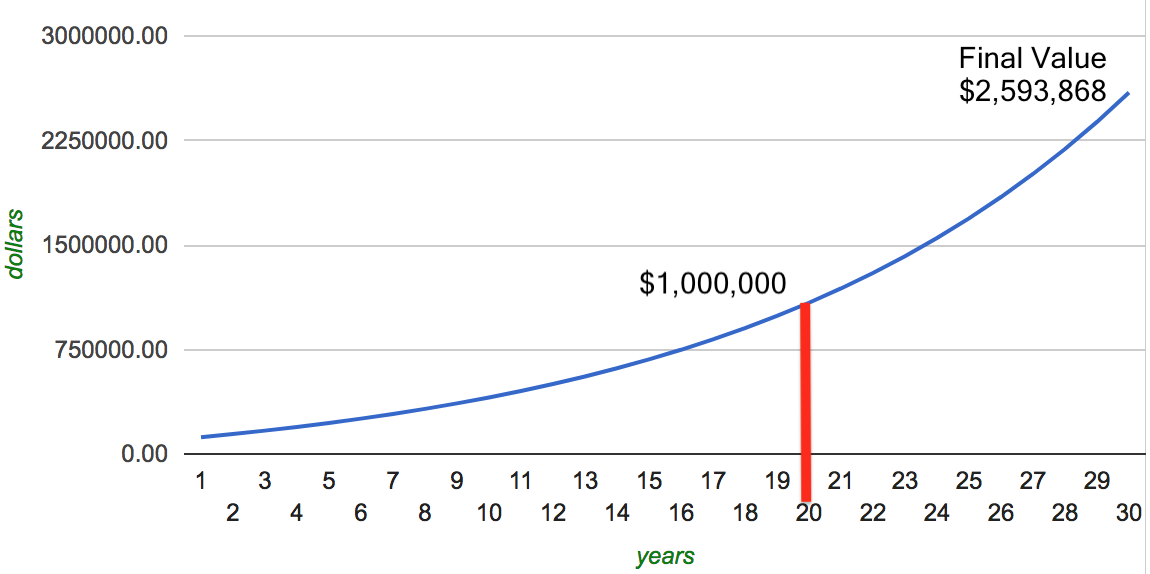

So let’s use numbers to talk about why all this matters. You start with $100,000 and invest $1,000 per month for 30 years. You don’t hire an advisor, because studies show that passively managed index funds outperform actively managed portfolios. Let’s say you invest 100% in the Vanguard 2045 Retirement Fund (VTIVX). This fund has an expense ratio of .15%. You get a rate of return of 8%, here’s what growth might look like. You hit $1mil in year 20 and end up with $2,593,868 after 30 years. Let’s compare that with your managed portfolio that performed similarly, but had 1.5% more in fees. So the effective rate of return is 6.5% instead of 8%. Here’s what that growth would look like.You hit $1mil in year 23 and end up with $1,811,349. That 1.5% fee will cost you $782,000 over 30 years! I don’t have a good way to measure the impact of commissions/load fees, but just know that if your brokerage charges those, it’ll set you back even more.

Selecting a Financial Advisor

My simple opinion is that you shouldn’t use a financial advisor. Do research yourself, open a Vanguard account, buy low cost index funds, continue learning, and adjust strategy as necessary. I am a strong believer that nobody cares about my money more than I do.

There are lots of things difficult about choosing an advisor. To name a few…

- Not all financial advisors are created equal. If you know your stuff and meet with a financial advisor, it usually doesn’t take long to identify if they know their stuff or are selling terrible products.

- Most financial advisors won’t consistently outperform the market or their benchmarks. If someone tells you “I beat the market last year”, feel happy for them, but don’t assume that means they’ll beat it every or even most years. You’ll be investing your money for 20+ years. It’s pretty tough to know today if someone can guess correctly and outperform the market over 20 years.

- There is no guarantee your advisor will beat the market. I’d actually consider signing up with an advisor that says, “If I don’t beat the market after my fees, I will refund you the difference. If I beat the market, I’ll take 25% of the amount I beat the market by.” You won’t ever get that promise. In reality, you’ll pay a management fee regardless of how good or poorly your portfolio performs, as compared to the market or your benchmark.

- Performance often matters more than personality. Being in the financial world, I’ve met lots of people I really like, but unfortunately they don’t know their stuff. I’ve also met some great financial salesmen, but that doesn’t mean they are going to make sound financial decisions.

- Personality also matters! I think a good advisor is a good coach. They’ll call you out when you’ve slacked in your saving efforts and calm your nerves when you get anxious and want to do something crazy, like stop investing when the market is dropping.

- Your advisor may be great, but their company may be terrible. When I worked at Wells Fargo, I had an internal battle when I had to sell terrible products or was told to do something slimy. For example, a manager frequently encouraged us to run credit card applications for people without them even knowing about it. Plenty of good people succumbed to that pressure out of fear of losing their job. That manager still works for the bank doing compliance! Something similar could be going on at your advisor’s company.

There are plenty of good people in the financial planner, advisor, broker, or fiduciary space, but be extremely careful in giving up control of your finances. Also, realize that paying management fees will erode your long-time savings. Compound interest is a beautiful thing. Get as much of it as you can!

***Disclaimer: The information provided herein is for informational purposes only. It should not be considered legal or financial advice. You should consult with an attorney or other professional to determine what may be best for your individual needs. I don’t make any guarantee to any results. No one should make any investment decision without first consulting their own advisors and conducting his or her own research and due diligence.***