Occasionally, friends/clients ask if they should refinance so they can lower their mortgage payment. If interest rates have fallen, if you are trying to drop mortgage insurance and your current lender is playing hardball, or if you are just trying to lower your payment by extending your loan out further, then refinancing may be the right option. In other situations, recasting your mortgage could be a good alternative.

The average homeowner has probably never heard of recasting. I heard about it maybe 2 years ago, when a friend/client told me several of his colleagues would recast after receiving big bonuses or selling off big stock grants. He wanted to make sure his new loan had the option, for if/when he would do the same.

Here’s how it works…

Let’s say you bought a house 3 years ago with a $300,000 mortgage at 4% interest. Your principal and interest payments (P+I) should be $1,432.25. Today your loan balance has dropped to $280,000. Let’s say you’ve recently earned a bonus of (or saved) $20k, and you intend to use this to pay your mortgage down to $260,000. Before dropping the $20k payment, you can contact your lender and tell them you’d like to recast your loan with a $20k payment towards principal. Your lender will re-amortize your mortgage based off the new reduced balance. The interest rate does not change. Your loan term does not change (27 years still remain). But your P+I will be calculated off a $260,000 balance. This means your payment would drop from $1,432.25 to $1,313.54. Lower payments are cool!

The Fine Print

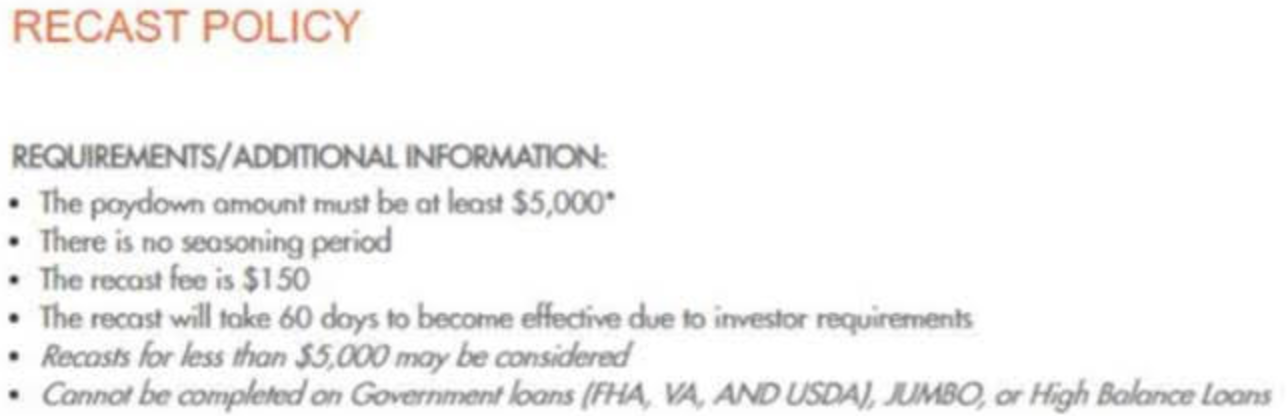

Here’s the fine print about recasting with one of the nation’s largest lenders:

The big things to note in my mind are:

- The lender charges a recast fee. In this scenario it’s $150.

- Recasts require $5,000+ paydown amounts.

- Recasts can’t be done on FHA, VA, USDA and some other loan types. It’s possible your specific jumbo loan may be eligible, but the government insured loans don’t allow it.

- The lender takes their sweet time to change your payment. 60 days with this lender.

Why would you want to do this?

One reality of recasting is that it won’t save you from any extra interest charges. The interest rate you started with, is the interest rate you’re going to end with. If you continued to make the same payment after you recast, you’ll pay off your loan at the same time as you would had you not recasted.

Here’s the difference though… the REQUIRED monthly payment goes down. Assuming you’d make the $20k principal payment whether you recast or not, it may be nice in the future to have added flexibility with a lower payment.

Let’s say the home is a rental property, and you need to get your payments down to free up flexibility for future purchases. Refinancing could be expensive, especially if interest rates have risen. By recasting with that $20k, your payments would drop $118.71/month. That’s an extra $1400/year in cashflow.

Another situation I dealt with recently… The market was extremely hot in Salt Lake earlier this summer. Being so competitive, it was difficult to find sellers willing to accept an offer that was contingent on the buyer having to first sell their old home. With so many anxious buyers, they didn’t want to take one with that extra baggage and risk. I had a buyer that was interested in a $750k home. They were able to qualify for the new purchase without first being required to sell their current home. The buyer had maybe 15% to put down on the new house, but was not interested in having a $637k mortgage. They had about another $150k in equity in their old home. My suggestion… We could put an offer on the new house without a previous home sale contingency. Once accepted and they’re confident moving forward on the new purchase, we could list their old home for sale. After closing on the new house, they could take their time a little more to make repairs and get settled in. After their old home sells, they could take their $175k, recast their new loan with under a $500k balance, reduce their payment, and lose the mortgage insurance. My buyer loved that suggestion, and like most, didn’t know recasting was even an option.

I’ve had some retirees get excited about the recasting option after selling a secondary property, as it reduces their monthly expenses. At their age, they aren’t looking to put their cash at risk in index funds. They’d rather put the cash towards minimizing their expenses and preserving their wealth. Maybe there are additional reasons recasting would make sense for you.

Recasting and FI

I think many in the FI community may opt against recasting. There are a few ways to look at it… Liquidity seems to reign supreme with FI. Keep the $20k invested in index funds, and it’s not attached to an illiquid asset. If you apply the 4% rule to that same $20k, it would provide you with $800/year in income.

On the flip side, let’s assume you’re recasting the mortgage on a rental property. The $20k will reduce your annual debt servicing obligations, thereby increasing your cashflow by ~$1,400/year. A $20k investment that adds $1400/year of cashflow, is a 7% annualized cash on cash return for the life of that mortgage. Seems to beat the 4% rule… I think all us FIRE folks have varying ideas on how to arrange our assets and liquidity. Pick your poison!