As a real estate agent I spend a lot of time looking at mortgage quotes. I think I spend more time than most agents, because I’m such a nerd about personal finances. That, and I want to make sure my buyers are getting a good deal. I think it’s an important part of my job.

I bought a house in July 2018 and my interest rate was 4.625%. In early 2019, rates really started to drop. In April, I refinanced down to 3.8% and I paid less than $400 to complete the refi. My payments are about $140 less per month. Best $400 I’ve spent. Since I got such a good deal, I had to share it with all my friends/clients that bought houses in the last couple years at a higher rate. Many of my friends asked me the same thing: “Which interest rate should I choose?”

You get what you pay for (sometimes)

Some people may not realize this, but you can get pretty much whatever interest rate you want. Let’s say you ask your loan officer (LO) to send you a quote. Odds are, the quote you’ll get is for the “par rate.” A par rate is the going rate without paying extra fees to get a lower rate or receiving lender rebates to take a higher rate. Let’s say the par rate is 4.25%. If you tell the LO you are looking to get 4% interest, they may tell you “we can do 4%, but it’s going to cost you an extra $3,000 in points at closing.” If you say you want 4.5%, your LO may tell you “we can do that, and we’ll give you $3,000 of credits at closing.”

Let’s talk about how to evaluate the cost/value of choosing an interest rate. My mortgage broker sent this chart to one of my clients:

Notice that as the rate goes up, the payment goes up, and the Points (aka closing costs) column goes down. A single Point is 1% of the loan amount. On a $300k loan, 1 point would be $3,000 in fees just for the rate you selected. 1/2 point would be $1,500.

If you were to select 3.75% instead of 3.875%, it will cost you $1,917.54 (1162.77+754.77) extra at closing, but save you $22.64 (1495.35-1472.71) in your monthly payment. This means it would take you 84.7 months (1917.54/22.64), or 7 years, before you’ve saved more through your monthly payments than the cost you paid upfront. I call this the payback period. In my experiences, a 7 year payback period is pretty typical when you pay to drop your interest rate. I always encourage buyers to calculate their payback period when considering different rate options.

Is it worth it?

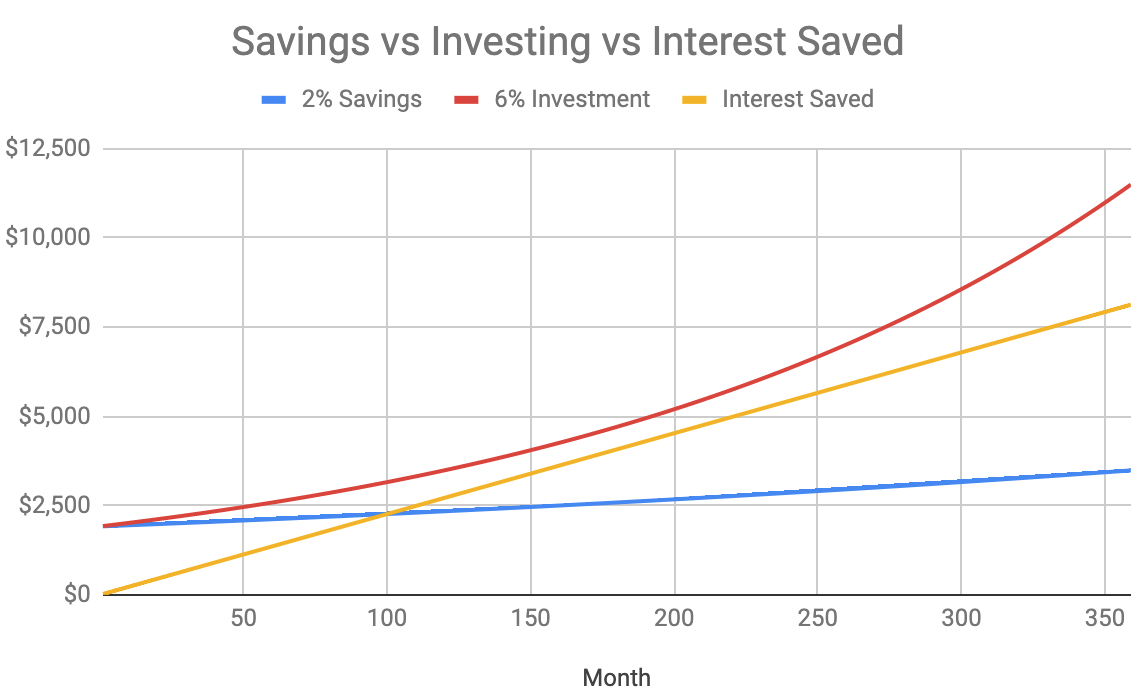

Is it worth paying $1917 now to save $22.64 per month? In my opinion… No, it’s not usually worth it. It takes 7 years before you’ve made up the extra cost. If you put the $1917 into a a savings account with 2% APY, it takes 8.5 years. Will you even own the house for that long? Will rates drop and cause you to want to refinance? If you invest the $1917 and get a 6% (or anything above 3.875%) return, you’ll certainly be better off taking the $1917. Below shows the growth of your cash vs savings over the life of a 30 year loan.

With 6% annualized growth, you’d never be ahead on your $1917 savings.

The above scenarios require discipline. If you don’t plan to take your savings at closing and depositing and keeping them in a savings or investment account, then disregard everything here. Maybe you plan on taking your $1917 in savings and buying furniture. That’s fine. Just not the focus of this post.

When you may choose the different rate options

There are plenty of situations where it can make sense to buy down your rate, or even take a higher rate.

Choosing a higher rate… A client of mine will be closing on a new home in a few weeks, and he is choosing a higher interest rate, so he has minimal out of pocket costs at closing. He is only making a 3% down payment, will be fixing up the house, and plans to refinance in 6-9 months when he has more equity. There’s no sense in him paying upfront for a lower interest rate, because he won’t have the loan long enough to make up for the extra upfront cost.

Choosing a lower rate… Let’s imagine that rates are at or near an all-time low, and you are buying a house you plan to own for 20+ years. It may make good sense to pay a little bit upfront to get a lower interest rate. Because rates are low, it is unlikely you’ll be able to refinance later at a lower interest rate. Because you will own the home for 10+ years, you’ll make enough monthly payments to earn back the costs you are paying upfront for a lower rate. It may be a good idea to buy down the rate now.

There are a myriad of other scenarios where it may make sense to take a higher or lower rate than the par rate. However, I think the par rate often makes the most sense.

Make sure you’re getting a good deal

I mentioned in a previous post that not all mortgage lenders are the same. Pricing can vary drastically from one to another. If you only speak to one lender, odds are you could save $1000s by shopping their rate around to one or two other lenders. They can all charge different fees and say they have different par rates. Feel free to ask me for a mortgage referral, and I’ll see if I know/can find a well-priced and reputable one in your area. Or get in touch with a local real estate agent that you trust will understand this stuff.