WARNING, this post may be more dry than some others… Lots of numbers and charts… It may not be as entertaining or short as my other posts. But if you apply what I’m saying, it’ll likely save you a few thousand dollars the day you sign for your next home purchase… and maybe a little bit every month thereafter on your mortgage payments.

Homebuyer Negotiations

As a Realtor, just about every buyer I know tries hard to negotiate down the price of their new home. As they should! HOWEVER, few people seem as concerned/aware about the price of their mortgage. In reality, you should probably be more concerned about negotiating price on your mortgage than negotiating $2-3k off your home price. It’s much easier to negotiate too. Every $1,000 on your purchase equates to about $5/month on a 30 year loan at 4.5% interest. As a homebuyer, you have an ocean of lenders wanting to sell you a loan. Make them fight for it a little bit. I saved over $5k at closing by negotiating with different banks on my last mortgage. A lower interest rate also saved me about $18/month.

Examples

I built a new home in 2018. A beautiful townhome that I’ll probably turn into a rental in the next 18 months. The builder required I get qualified with their preferred lender. Aside from them, I had 2 of my go-to lenders give me quotes before deciding who I’d work with. All 3 were given the same info (purchase price, down payment amount, credit score, and closing date).

Here is a blurb of what my first quote looked like from the preferred lender (Lender A) and the following blurb is from Lender B that I ended up choosing:

Summary – Lender A | $3,391 in lender-specific fees | No lender credit | $5,258 final cost

Summary – Lender B | $1,093 in lender-specific fees | $2,750 lender credit | $1,424 final cost

In between those 2 quotes, I had another from Lender C, then I asked all 3 to beat the best prices. This maybe took 3-4 hours total of my time. Also, Lenders A and C were at 4.75% while B was 4.625%. If you sum up each line item from those quotes, the total from Lender B is $3,834 less and equates to about $20 less on my monthly payment. Seems obvious to go with Lender B’s quote, right?!

NO, it’s not all obvious! Several line items above don’t need to be considered when comparing loan quotes. In reality, Lender B’s was actually $5,048 lower in fees! Lender A was going to charge me $3,391 to use them. At the same interest rate others were offering, Lender B gave me $1,657 in CREDITS to use them.

Things to look for

There are likely 20+ line items on any full mortgage quote. Here are the parts to focus on when comparing:

- Lender Fees (or Credits)

- Interest Rate

- Monthly Mortgage Insurance (if applicable)

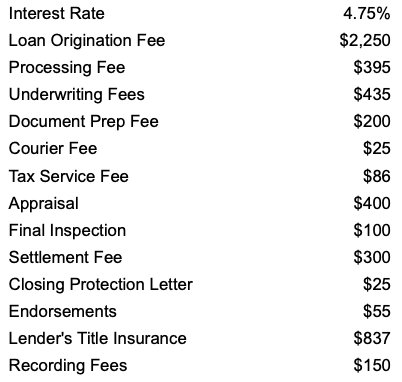

2 and 3 are easy to spot. Number 1 can be tricky, and you may need a trained eye to identify them. Here are disguised lender fees or credits from the quotes above:

Loan origination fee, processing fee, underwriting fee, document prep fee, courier fee, tax service fee, appraisal fee, final inspection, flood determination, flood life of loan, and lender credits.

Wow, that’s exhausting!

All other line items in there are estimates of 3rd party fees that will be the same regardless of which lender you choose. These fees are most often paid to your title company, attorney, insurance company, county or city, HOA, or real estate broker. The lender has no control over what these third parties charge, but they still try to estimate them in their quotes. Sometimes estimates are way off, and it can disguise a bad quote as a good one.

I consider it my job to help buyers find the right lender and help them negotiate good mortgage pricing. I’m certain many Realtors don’t give this the same attention I do. Find one that will.

It may seem obvious to “get a good deal”, but from my experience, most mortgage buyers don’t know a good one from a bad one. Lender A said about 40% of buyers don’t shop around or negotiate. This makes me sick to my stomach, especially because Lender A eventually came down almost $4k and .125% from their original quote. This confirms to me that many buyers don’t know a good mortgage deal from a bad one.

Do Your Homework

Here are some things that help in the negotiation process:

- Be a good borrower: Many lenders give best rates to those with 760+ credit scores. Lenders typically give better pricing at 25% down and again at 40% down. Be aware of the different pricing thresholds, even if you’re not looking to put a lot of cash down. First-time homebuyers making UNDER a certain amount can also qualify for improved pricing.

- Compare apples to apples: Every lender has the option to increase upfront fees to have a lower interest rate or monthly payment. Don’t think that one deal is better than another because just fees are lower or just the interest rate is lower. Ask each lender to give you a quote at the same interest rate. It also helps to get the quotes on the same day, because rates will fluctuate daily.

- Extra perks: This won’t always be a factor, but some banks/credit unions offer additional incentives based on products you have with them. At Chase, I once got 75,000 Ultimate Rewards points after getting a mortgage, because I also had a specific credit card. Citi offers interest rate discounts based on balances. See/ask what incentives they offer if you have or open other products at the institution.

- Know your lender: Sometimes you can get what you pay for. Great service may be worth paying a little extra, and it will likely save you time. I’ve seen some budget lenders that require mortgage payments by check in the mail. Some are notorious for making errors with county taxes or escrow accounts. Some credit unions have killer pricing, but are notorious for not closing on time. Not closing by your contract dates could cost you late fees or, even worse, lose you the deal. Mortgages are notorious for being sold. I like when my mortgages end up at Chase, Wells Fargo, or other large banks. It may be worth asking your lender where your mortgage is going to end up.

- Shopping lenders will not destroy your credit: The CFPB has said: “Within a 45-day window, multiple credit checks from mortgage lenders are recorded on your credit report as a single inquiry.” This allows you to shop each lender in a short window of time. If a lender tells you otherwise (and some will), they’re probably trying to scare you/play hardball so you don’t keep shopping.

Bottom Line

There is a lot more that could be said about shopping for a mortgage. If you are trying to buy a house and will be getting a mortgage, it will pay to know what you’re doing. If you don’t have a partner or fiduciary you trust, feel free to reach out and I’ll give you my free and honest opinion.

And since this post was more stale than some others, a witty mortgage/real estate clip from Arrested Development. #NINJAplease

Pingback: Should I buy down my mortgage interest rate? | Salary Optional